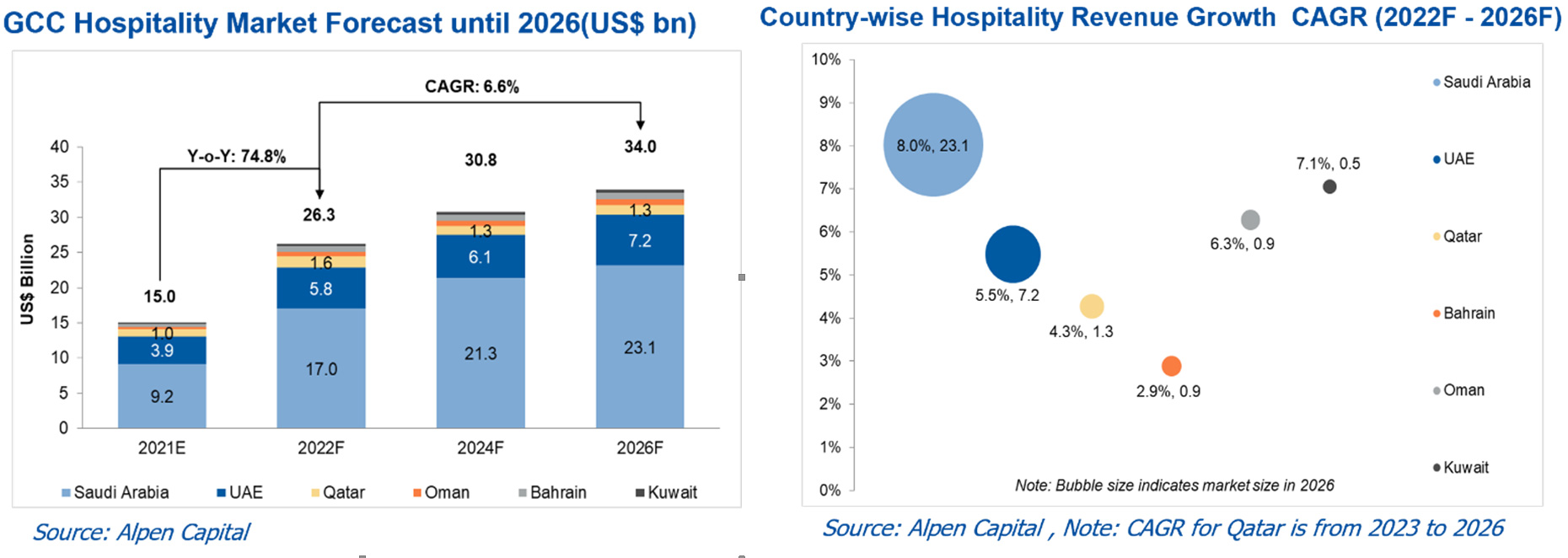

According to Alpen Capital, the GCC Hospitality industry revenues are forecasted to grow at a pace of 6.6% CAGR between 2022 and 2026 to reach US$ 34.0 billion. Strategies adopted by the regional governments, economic recovery, increase in tourist arrivals along with innovative solutions being offered by the operators are primary drivers of growth for the industry.

Growth in the hospitality sector revenue of individual GCC countries is expected to range from a CAGR of 2.9% to 8.0% between 2022 – 2026. Largest markets in the GCC, Saudi Arabia and UAE, are expected to witness CAGRs of 8.0% and 5.5%, respectively. Kuwait, Oman and Bahrain are expected to grow at 7.1%, 6.3% and 2.9%, respectively. Whereas growth in Qatar is expected to normalize post the completion of the FIFA World Cup 2022 with a CAGR of 4.3% between 2023-2026.

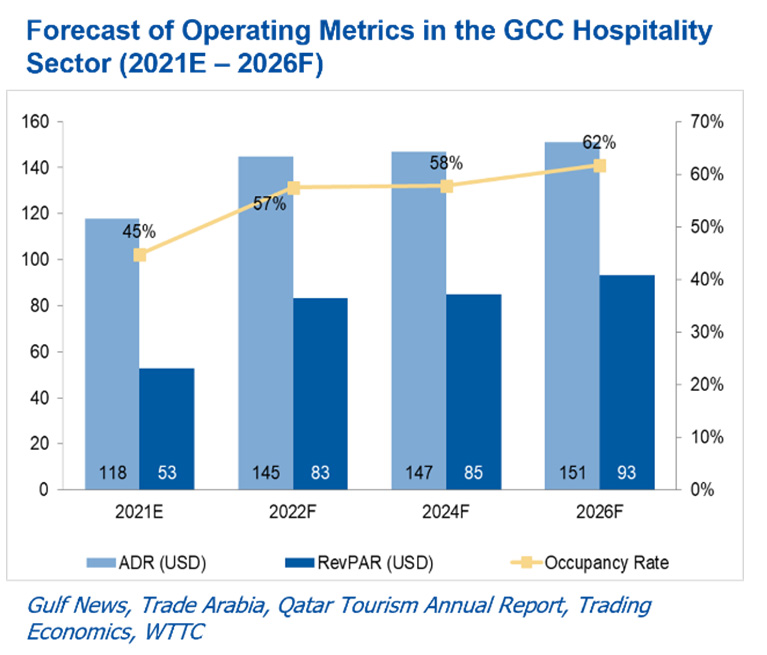

After witnessing a significant increase this year, the hospitality operating metrics are likely to witness steady growth going forward. Average occupancy rate across the GCC is forecasted to rise from 57% in 2022 to 62% in 2026. The Average Daily Rate is forecasted to increase from USD 145 this year to USD 151 in 2026, whilst Revenue Per Available Room is expected to increase from USD 83 to USD 93 representing an annualized growth rate of 1.1% and 2.9%, respectively.

Business confidence in the region is bouncing back quicker with the reopening of borders and easing of travel restrictions. GCC is fast becoming a global center for business, entertainment, and sporting events, and is set to host major events like FIFA World Cup 2022, Formula 1 Grand Prix, World Aquatics Championship, Geneva International Motor Show Qatar, Asian Games, etc. Moreover, improvements in per capita income will increase domestic consumer demand which will continue to help boost the tourism sector. GCC countries are also upgrading their transportation ecosystem, from expanding airport capacity to adopting Hyperloop-based transport and a new railway corridor. They have been actively investing in developing tourism-related infrastructure while promoting leisure destinations. Saudi Arabia, especially, has undertaken several socio-economic reforms to make the Kingdom more modern, liberal, and business and tourism friendly to increase its attractiveness for international tourists.

However, the report also notes that global inflation, sharp adjustments in oil prices and revenue pose threats to the industry. The high rate of inflation is likely to impact consumer spending power, whilst travel could also be impacted by uneven vaccination rates and new COVID-19 strains.

The Covid-19 outbreak required the region’s hospitality sector to diversify its offering to remain competitive and relevant to attract visitors, and the industry responded with innovation and vibrant new business models. Notable trends include the introduction of mid-scale brands and serviced apartments, with digitization helping operators streamline workflows, reduce costs, and enhance customer experience. The Airbnb model has also started gaining considerable ground in the GCC, the Alpen report stated. Religious tourism continues to play a significant role and growth in the number of pilgrims has compelled Saudi Arabia to offer a wide range of hospitality services. Other states are adopting distinct models of engagement between heritage and religious spheres to attract tourism. Going forward the GCC hospitality industry is expected to emerge stronger from the crisis, ahead of its peers.

To download the report, please click here.

Back

Back